Quick Answer: Yes, you for sure can refi without the need for tax returns and use alt income doc options like asset based lending, bank statement loans and DSCR loans. STX lending has helped hundreds of families buy homes that were self employed, business owners and real estate investors. It surprises most, but there are many more options than people think out there.

Can You Refinance Without Tax Returns?

The need for reviewing tax returns when applying for a home loan is only really required when your trying to do a loan backed by the FHFA (Federal housing and finance administration). This means they follow the rules of Fannie Mae, Freddie Mac and Ginnie Mae (For government loans).

Bank Statement loans: This has been the go to alternative loan whether its a mortgage refinance or home purchase when looking at alternative options. You need to find a lender (Like us! ) that will allow you to calculate the income off 12 – 24 months of bank statements (personal or business) and calculate your income that way. Getting a CPA to confirm your expense factor can even let you count more of the income as well.

Why You Might Need Alternative Income Documentation

Self Employed Challenges with Traditional Mortgage Requirements

Business Write-Offs Impact Reported Income : Self employed borrower are usually taking legit tax deductions so that it really reduces the taxable income they are taxed on. The CPA will max out the deductions like depreciation, vehicle expense and operating expenses like meals. These are all normal , but reduce your ‘net income”

When a traditional lender analyzes returns that max out deductions on your 1040 or 1120s, they may think your struggling financially, when in reality its the exact opposite.

Unfiled Tax Returns Some borrowers have unfiled tax returns due to:

- Recent career changes from W-2 employee to self employment

- Complex business situations requiring extended tax preparation time (I’ve seen CPA firms take 6+ months on complicated returns)

- Financial hardship that prevented timely filing

- Divorce proceedings where tax documents are disputed

- Honestly, sometimes just procrastination (hey, it happens to the best of us)

Types of Alternative Income Documentation Mortgages

Bank Statement Loans: Most Popular Option

Bank statement loans have become the go-to solution for self employed borrowers who need to refinance without providing tax returns to mortgage lenders. This is probably 80% of what we do for alternative documentation these days.

How Bank Statement Loans Actually Work:

- Provide 12-24 months of personal or business bank statements (I usually recommend 24 if your income’s been climbing)

- Mortgage lenders calculate average monthly deposits as qualifying income

- Lenders typically use 50-75% of deposits to account for business expenses, depending on your industry

- Available for both rate-and-term refinance and cash-out refinance options

For example, if your business account shows $10K average monthly deposits, they might qualify you on $6,500-7,500 monthly income. Still way better than what your tax return probably shows after all those write-offs.

Bank Statement Loan Requirements:

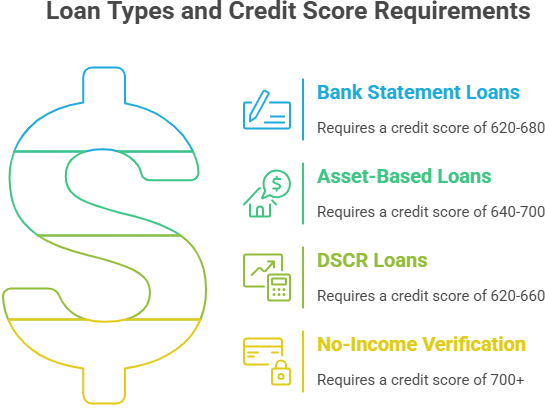

- Minimum credit score: 620-640 (though I’ve gotten people approved with 600 in the right circumstances)

- Debt to income ratio: Up to 50% accepted by many lenders (vs. 43-45% for conventional)

- Down payment/equity: 20-25% minimum for refinance, 25-30% for cash-out

- Self employment history: 2+ years preferred by most lenders

- Those bank statements better tell a consistent story – no wild swings or unexplained gaps

The rates? Yeah, they’re a bit higher – usually 0.5% to 0.75% above conventional rates. But if it’s the difference between getting approved and getting denied, that math works out pretty well.

Asset-Based Loans for High Net Worth Borrowers

I don’t do tons of these, but they’re perfect for certain situations. Think retired business owners with huge investment accounts but no traditional income, or trust fund folks who don’t technically “work” but have substantial assets.

How Asset Qualification Works:

- Total liquid assets divided by loan term (typically 360 monthly payments)

- Creates qualifying income figure for mortgage approval

- Example: $720,000 in assets ÷ 360 months = $2,000/month qualifying income

Honestly, these loans feel a bit like cheating (in a good way). The lender basically takes your liquid assets, divides by the loan term, and calls that your income.

Acceptable Assets:

- Checking and savings accounts

- Investment portfolios and retirement accounts

- CDs and money market accounts

- Stock portfolios and mutual funds

Credit score requirements are higher – usually 680+ – and you’ll need substantial assets. But if you qualify, it’s probably the easiest loan process you’ll ever experience.

DSCR Loans for Investment Properties

This is the most common use of a DSCR mortgage loan. DSCR loans are specifically design for investors who want to refi investment homes without the need of showing their tax bill, making it the best possible options for self employed business owners.

How DSCR Loans Work:

- Loan approval based purely on property’s rental income potential

- Appraiser provides fair market rent analysis during the appraisal process

- Property income must cover mortgage payment (ideally 1.25x or higher)

- No personal tax returns or employment verification required whatsoever

I love these because the math is straightforward. If the property rents for $2,000 and the mortgage payment would be $1,500, you’ve got a 1.33 DSCR – which means the deal makes sense. Most lenders want to see at least 1.0, better if it’s 1.25+. Real estate agents can also calculate this pretty easily.

Fair warning though: These work great for experienced investors, but if you’re buying your first rental property, you might struggle to find a lender. They want to see you know what you’re doing.

No-Income Verification Loans

A Tax attorney should be aware of this type of loan as no sufficient income personally is needed to verify. Since financial institutions that do these have no income verification it eliminates the need to document income entirely.

Key Features:

- No employment verification required

- Qualification based on credit history and sufficient assets

- Higher down payments required (typically 30%+)

- Available for primary residence and second homes

Refinance Without Tax Returns: Requirements and Qualifications

Credit Score Requirements

Most alternative income documentation mortgages require higher credit scores than traditional mortgage options. Here’s what I typically see:

Higher scores obviously get better rates and terms. I’ve had clients with 750+ credit scores get pricing that’s almost as good as conventional loans.

Down Payment and Equity Requirements

Alternative documentation loans typically require more equity than traditional mortgages, which makes sense from the lender’s risk perspective:

- Refinance Equity Required: 20-25% minimum

- Cash-Out Refinance: 25-30% equity must remain after cash-out

- Investment Properties: 25-30% down payment minimum

- Primary Residence: 20-25% down payment minimum

Debt to Income Ratio Flexibility

One big advantage of alternative income documentation is higher debt to income ratio acceptance:

- Traditional Mortgages: 43-45% maximum DTI (pretty rigid)

- Bank Statement Loans: Up to 50% DTI accepted (much more realistic)

- Asset-Based Loans: DTI calculated differently using asset depletion method

- DSCR Loans: No personal DTI requirement at all

Mortgage Lenders Who Offer Alternative Documentation

Non-QM Lenders vs Traditional Lenders

When submitting a loan application, most traditional mortgage lenders who sell to Fannie and Freddie won’t offer an alternate loan option. Same goes for govy loans that are traditional loan options based, DSCR or NonQM is not an option. Thats where a Non QM home loan come into play.

Types of Lenders:

- Portfolio Lenders: Keep loans in-house, maximum flexibility on guidelines

- Non-QM Specialists: Focus specifically on alternative documentation loans

- Credit Unions: Sometimes offer portfolio loan options (can be surprisingly flexible)

- Private Lenders: Highest flexibility but potentially higher rates

What to Look for in Alternative Documentation Lenders

After doing this for years, I’ve got strong opinions about who’s actually good at alternative doc loans versus who just claims to be.

Experience with Self Employed Borrowers

- Ask about their approval rates for bank statement loans specifically

- Verify they understand business bank statements analysis (some lenders have no clue)

- Ensure they’re familiar with self employed income calculation methods

Local Market Knowledge

- Choose mortgage lenders familiar with your local market conditions

- Look for established relationships with local appraisers who understand property values

- Prefer lenders with local underwriting teams (faster communication)

Red flags to watch for:

- Lenders who promise things that sound too good to be true (they usually are)

- Anyone who can’t explain their underwriting process clearly when you ask

- Companies that want significant upfront fees before doing any real work

Credit unions can be surprisingly flexible, especially if you’ve got history with them. I’ve had great luck with some of the regional banks too – they keep loans in portfolio and can bend rules that national lenders can’t.

Pros and Cons of Refinancing Without Tax Returns

Advantages of Alternative Income Documentation

Flexibility for Self Employed Individuals

- No need to wait for tax return preparation or filing

- Actual cash flow recognized vs. artificially low reported income

- Works with complex business structures and multiple income sources

- Doesn’t penalize you for smart tax planning and legitimate deductions

Faster Approval Process

- Less documentation to gather and verify upfront

- Streamlined underwriting for qualified borrowers who fit the program

- Can close in 30-45 days vs. 45-60 for traditional mortgages

- No back-and-forth about explaining business deductions to underwriters

Privacy Protection

- Keep detailed financial information private

- No need to explain business deductions or tax strategies to some mortgage professional

- Minimal documentation requirements compared to conventional loans

Disadvantages to Consider

Higher Costs

- Interest rates typically 0.25% – 1.25% above traditional mortgage rates

- Additional fees and origination costs (usually 0.75% to 1.25% vs. 0.5%)

- Potentially higher closing costs due to specialized processing

Let’s be honest about the money because that’s what you really want to know. On a $300K loan, that extra 0.5% costs you about $125 monthly. Over the life of the loan, yeah, it adds up. But compare that to being stuck with a high-rate loan you got years ago, or not being able to refinance at all.

Limited Lender Options

- Fewer mortgage lenders offer these programs

- May require specialty Non-QM lenders (more limited shopping)

- Less competitive rate shopping compared to conventional loans

Stricter Qualification Requirements

- Higher credit score requirements across the board

- Larger down payment needs

- More stringent asset verification and reserves

Tax Lien and Unpaid Taxes Considerations

Impact of Tax Debt on Refinancing

This gets messy fast, so I’ll keep it real with you. Having unpaid taxes or a tax lien doesn’t automatically disqualify you from refinancing, but it definitely creates additional complications:

IRS Payment Plans

- If you have an established payment plan with the IRS, many lenders will treat it as monthly debt in your debt to income ratio

- Payment history on IRS installment agreements is crucial – you need to be current

- Some lenders require the payment plan to be established and current for 12+ months

Tax Lien Subordination

- For cash-out refinance, you may need IRS lien subordination

- Tax lien subordination allows your new mortgage to take priority over the IRS lien

- This process can add 30-60 days to your closing timeline and isn’t guaranteed

Working with Tax Professional

Before applying for any mortgage refinance with tax issues, I always recommend:

- Consult with a tax attorney or CPA about your specific situation

- Understand all options for resolving unpaid taxes before applying

- Get written confirmation of payment plan status from the IRS

- Consider whether paying off tax debt improves your refinance options

My honest advice? If you’ve got serious tax issues, deal with those first if possible. It opens up way more lending options and usually saves money in the long run.

Frequently Asked Questions

Can W-2 employees refinance without tax returns?

Yes, traditional employees can sometimes refinance without providing tax returns by using recent pay stubs, W-2s, and bank statements. However, most traditional mortgage lenders will still request tax returns for complete income verification.

Honestly, if you’re a W-2 employee, you probably don’t need to go the alternative documentation route unless there’s something unusual about your situation.

How much equity do I need to refinance without tax returns?

Most alternative income documentation loans require 20-25% equity for rate-and-term refinance and you need to keep 25-30% equity after a cash-out refinance. Investment properties may require 25-30% equity minimum.

What credit score do I need for bank statement loans?

Minimum credit scores for bank statement loans typically range from 620-680, depending on the lender and other qualifying factors. I’ve gotten people approved with 600 in the right circumstances, but 640+ gives you much better options.

Higher credit scores may qualify for significantly better interest rates and terms – sometimes the difference is substantial.

Can I refinance investment properties without tax returns?

Absolutely, and this is actually one of the easiest scenarios. DSCR loans are specifically designed for real estate investors to refinance investment properties without any personal income documentation. The property’s rental income potential is all that matters for qualification.

How do lenders verify income from bank statements?

Mortgage lenders analyze deposit patterns over 12-24 months, remove irregular or one-time deposits (like tax refunds or loan proceeds), and apply expense factors (typically 25-50%) to determine qualifying income from bank statements.

They’re looking for consistent deposits that represent actual business income, not just money moving around between accounts.

Are there prepayment penalties on alternative documentation loans?

Some Non-QM lenders include prepayment penalties, typically lasting 1-3 years. Always review loan terms carefully and ask specifically about prepayment penalty clauses before signing anything.

Not all alternative doc loans have prepayment penalties, but enough do that you need to ask upfront.

Can I refinance with unfiled tax returns?

Yes, bank statement loans and other alternative documentation options don’t require filed tax returns at all. However, having tax debt or IRS issues may create additional complications that need to be addressed separately.

What’s the difference between bank statement loans and no-doc mortgages?

Bank statement loans require bank statements as income verification, while true no-doc mortgages require minimal documentation. Both are alternatives to traditional tax return mortgages, but bank statement loans are much more widely available and generally have better terms.

True no-doc loans are pretty rare these days and usually come with significantly higher rates.