Are you a Texas homeowner looking to tap into your property’s equity? Thinking about renovating your home, paying off high-interest debt, or covering a big life expense? A Home Equity Line of Credit (HELOC) could be a smart way to know your home’s value. But if you live in Texas, it’s important to understand that

Introduction

Are you a Texas homeowner looking to tap into your property’s equity? Thinking about renovating your home, paying off high-interest debt, or covering a big life expense?

A Home Equity Line of Credit (HELOC) could be a smart way to know your home’s value. But if you live in Texas, it’s important to understand that the rules are different from other states. This easy-to-follow guide breaks down everything you need to know about getting a HELOC in the Lone Star State.

South Texas Lending (STX Lending), an experienced Texas-based lender, can assist you in navigating the state’s specific requirements, allowing you to safely access your home equity and avoid surprises along the way.

Key Takeaways

- In Texas, you can only borrow up to 80% of your home’s value with a HELOC.

- HELOCs in Texas are only available for your primary home, not investment properties.

- After applying for a HELOC, Texas law requires a 12-day waiting period before closing. This gives you time to review the terms.

- South Texas Lending team offers competitive HELOC rates and a smooth, efficient approval process.

- Most Texas homeowners need a 620+ credit score, 20% equity, and a reasonable debt-to-income ratio to qualify.

What is a HELOC and How Does it Work?

A Home Equity Line of Credit, or HELOC, offers a way for homeowners to borrow money using the equity they’ve built up in their property. Unlike a traditional home equity loan that provides a lump sum, a HELOC functions more like a credit card with your home as collateral.

Key Features of a Texas HELOC

- Revolving Credit Line: Borrow as needed, up to your approved limit, during the draw period.

- Draw Period: Usually lasts 10 years, giving you access to funds when you need them.

- Repayment Period: Usually 20 years after the draw period ends

- Variable Interest Rates: Rates typically fluctuate based on market conditions.

- Interest-Only Payments: Many HELOCs let you pay only the interest during the draw period.

- Minimum Draws: In Texas, your initial draw must be at least $4,000.

HELOC Structure and Timeline

A HELOC typically has two distinct phases:

- Draw Period (Usually 10 years)

- Access funds up to your credit limit whenever you need it.

- Make interest-only payments on the amount you’ve borrowed.

- Repay and reborrow as often as you like (within your limit).

- Repayment Period (Usually 20 years)

- No more withdrawals allowed.

- Begin paying back principal plus interest.

- Monthly payments may go up when this phase begins.

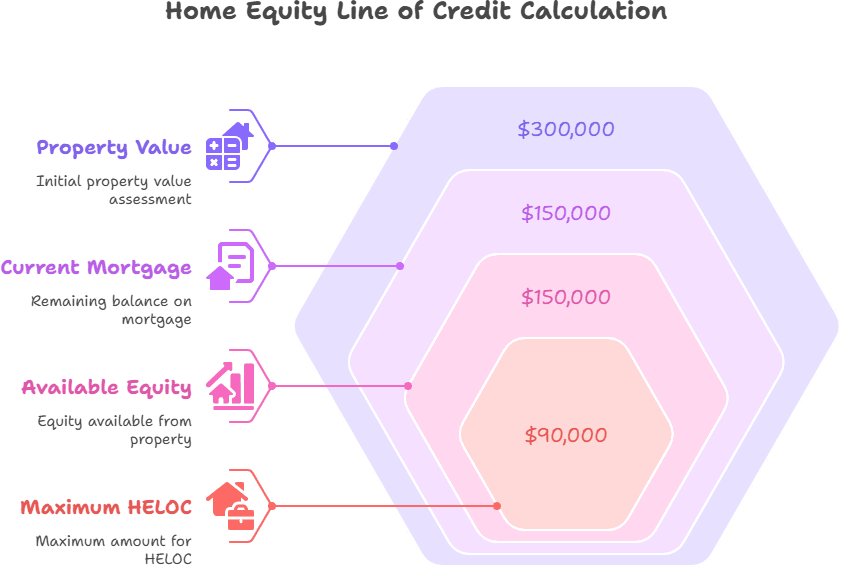

Real-World HELOC Example

Here’s an example to help explain how a HELOC works:

Property Value: $300,000

Current Mortgage: $150,000

Available Equity: $150,000

Maximum HELOC (80% LTV Rule):

$300,000 × 80% = $240,000 total allowable liens

$240,000 – $150,000 (existing mortgage) = $90,000 maximum HELOC amount

If this homeowner is approved for the maximum amount and opens a $90,000 HELOC, they:

- can borrow up to $90,000 during the 10-year draw period

- can borrow $50,000 and repay $20,000, increasing their available credit to $60,000

- will pay approximately $312.50 per month in interest-only payments on a $50,000 balance at a 7.50% interest rate

- will begin making payments on both principal and interest once the draw period ends

Texas-Specific HELOC Rules and Regulations {#texas-heloc-rules}

Texas has some of the nation’s most conservative home equity lending laws, designed to protect homeowners from over-leveraging their properties. These regulations make Texas HELOCs different from the other states.

80% Loan-to-Value (LTV) Restriction

In Texas, your mortgage and HELOC combined can’t be more than 80% of your home’s appraised value. This is more restrictive than many other states that allow up to 85-90% LTV.

Example Calculation:

- Home Value: $400,000

- Current Mortgage Balance: $200,000

- Maximum Possible HELOC: $120,000

- ($400,000 × 80% = $320,000) – $200,000 = $120,000

Primary Residence Requirement

In Texas, you can only get a HELOC on your primary residence (homestead property). Investment properties, second homes, and rental properties do not qualify for Texas HELOCs.

One Equity Loan at a Time Rule

Texas law allows only one home equity loan or HELOC at a time. If you already have one, you must pay it off completely before you can take out a new one.

12-Month Seasoning Requirement

After getting a HELOC in Texas, you must wait at least 12 months before you can refinance it or apply for another home equity loan.

Mandatory Waiting Periods

- 12-Day Cooling Off Period: Texas law requires a 12-day waiting period from the time you apply for a HELOC to when you’re allowed to close on the loan.

- 3-Day Right of Rescission: After closing, you have three business days to cancel the HELOC without penalty.

Fee Limitations

Texas limits closing costs to no more than 2% of the total loan amount (excluding appraisals, surveys, title insurance, or property tax-related fees).

Mandatory Closing Location

To finalize a HELOC in Texas, you must sign the paperwork in person. The closing must be done at the lender’s office, a title company, or an attorney’s office.

$4,000 Minimum Initial Draw

When you open a HELOC in Texas, your initial draw must be at least $4,000.

To qualify for a HELOC in Texas, you’ll need to meet several requirements. For example, here’s what South Texas Lending look for:

Credit Score Requirements

Most Texas HELOC lenders, including South Texas Lending, require a minimum credit score of 620. If you want more competitive rates, aim for a score of 700 or higher.

Home Equity Requirements

You need to have at least 20% equity in your home. This aligns with the 80% maximum LTV rule discussed earlier.

Income and Debt-to-Income (DTI) Ratio

Lenders typically look for a maximum DTI ratio of 43% or lower. This means your total monthly debt payments (including the potential HELOC) should not exceed 43% of your gross monthly income.

Example:

- Monthly Gross Income: $10,000

- Maximum Acceptable Monthly Debt: $4,300

- If existing monthly debts = $3,500, your HELOC payment can’t exceed $800

Property Requirements

To qualify for a Texas HELOC, your property must be:

- your primary residence (homestead)

- a single-family home, condo, townhouse, or certain planned unit developments

- located in Texas

Mobile homes, manufactured homes, and investment properties do not qualify for HELOCs in Texas.

Employment and Income Stability

Lenders prefer borrowers with:

- at least two years of consistent employment

- stable, verifiable income

- good payment history on existing loans

The HELOC Application Process in Texas

Getting a HELOC in Texas involves a few steps and usually takes about 30-45 days from application to funding. This timeline includes the state’s required waiting periods.

Step 1: Preparation and Pre-Qualification

Before applying, check your credit score, estimate your home’s value, and calculate your debt-to-income (DTI) ratio. You can use South Texas Lending’s online pre-qualification tool to see how much you can borrow.

Pre-Application Checklist:

- Review your credit report for errors.

- Gather recent financial statements.

- Calculate your home’s approximate value.

- Find out how much you still owe on your mortgage.

- Decide how much you want to borrow.

Step 2: Application Submission

You can complete South Texas Lending’s HELOC application online or in person. Be ready to provide the following:

- personal identification

- proof of income (pay stubs, tax returns)

- property information

- existing mortgage details

- information about other debts

Application Timeline Tip: Apply 45–60 days before you actually need the funds. As mentioned, Texas law includes mandatory waiting periods that can affect your timeline.

Step 3: Document Collection and Review

After you apply, you’ll need to provide:

- recent mortgage statements

- property tax records

- homeowners insurance documentation

- income verification (W-2s, tax returns, 1099s)

- asset statements (bank accounts, investments)

Document Submission Tip: Use our secure online portal to upload documents digitally. This speeds up the process.

Step 4: Home Appraisal

Most HELOCs require a professional appraisal to determine your home’s current market value. This appraisal establishes how much equity you have and your maximum borrowing amount.

Appraisal Process:

- Lender orders the appraisal through a third-party service.

- Appraiser sets up a time to visit to your property.

- They’ll evaluate your home’s condition and features.

- Your home will be compared to recent similar home sales in your area.

- You’ll get a final valuation report typically within 3-7 days after the inspection.

Step 5: Underwriting and Approval

South Texas Lending’s underwriting team will review your application, financial documentation, and appraisal to make a lending decision.

What Underwriters Evaluate:

- credit history and score

- income stability and amount

- debt-to-income ratio

- property value and condition

- loan-to-value ratio

Step 6: Mandatory 12-Day Waiting Period

Texas law requires a 12-day cooling-off period between application and closing. During this time, you’ll receive disclosures about the HELOC terms and your rights as a borrower.

Key Disclosures You’ll Receive:

- HELOC terms and conditions

- closing cost estimates

- your rights under Texas home equity laws

- important dates and deadlines

- right of rescission information

Step 7: Closing

Closing must take place at a lender’s office, attorney’s office, or title company. You’ll:

- review and sign loan documents

- receive copies of all signed papers

- pay any closing costs

- receive information about your 3-day right of rescission

Texas-Specific Closing Requirements:

- must occur in a lender’s, attorney’s, or title company’s office

- borrower must be physically present

- spouse must also sign (if the property is jointly owned)

- a notary must be present to witness signatures

Step 8: Funding and Access

After the 3-day rescission period, your HELOC becomes active. You can access funds via:

- online transfers

- checks linked to your HELOC

- a HELOC card (if offered by the lender)

- in-person withdrawals

Remember: In Texas, your first draw must be at least $4,000.

Visual Timeline of Texas HELOC Application Process

Average time from application to funding: 30-45 days

HELOC vs. Other Home Equity Options in Texas

Texas homeowners have several options for tapping into their home equity. Understanding the differences can help you choose the right financial solution.

HELOC vs. Home Equity Loan: Detailed Comparison

| Feature | HELOC | Home Equity Loan |

|---|---|---|

| Disbursement | Revolving credit line | Lump sum |

| Interest Rate | Variable (typically) | Fixed |

| Payment Structure | Interest-only during draw period | Fixed monthly payments |

| Flexibility | Borrow as needed | Receive all funds upfront |

| Initial Costs | May be lower | May be higher |

| Payment Predictability | Varies with rate changes | Consistent throughout term |

| Best For | Ongoing expenses, uncertain costs | Fixed expenses, known costs |

| Minimum Draw | $4,000 in Texas | Full loan amount |

| Tax Deductibility | Only for home improvements (under TCJA. Confirm current rules) | Only for home improvements (under TCJA. Confirm current rules) |

When a HELOC Makes More Sense

A HELOC might be the better option when:

- you need ongoing access to funds over time

- you’re unsure of the exact amount you’ll need

- you want the flexibility to borrow and repay as needed

- you’re comfortable with potentially variable payments

- you prefer lower initial costs

- you’re funding a project with multiple phases

Example Scenario: You’re planning a multi-stage home renovation that will occur over several years. A HELOC allows you to draw only what you need as each phase begins, limiting interest costs to the amounts actually borrowed.

When a Home Equity Loan Makes More Sense

A home equity loan might be better when:

- you need all funds upfront

- you want payment predictability

- you prefer a fixed interest rate

- you have a single, large expense

- you want to lock in current rates

Example Scenario: You’re consolidating $30,000 in high-interest debt and want a fixed payment schedule to ensure the debt is paid off within a specific timeframe.

HELOC vs. Cash-Out Refinance: Detailed Comparison

| Feature | HELOC | Cash-Out Refinance |

|---|---|---|

| Loan Type | Second mortgage | Replaces existing mortgage |

| Interest Rate Impact | Keeps current mortgage rate | Changes rate on entire mortgage |

| Closing Costs | Lower (on smaller amount) | Higher (on entire loan amount) |

| Term | Typically 30 years total | 15-30 years |

| Tax Implications | Deductible only for home improvements | May have broader deductibility |

| Rate Type | Usually variable | Fixed or variable options |

| Impact on First Mortgage | None – keeps original terms | Completely replaces original mortgage |

| Best For | Keeping a favorable first mortgage rate | When current rates are lower than existing mortgage |

Comparative Cost Analysis: $100,000 Borrowing Example

To illustrate the cost differences between these options, consider a Texas homeowner looking to access $100,000 in equity with a home valued at $400,000 and a current mortgage balance of $200,000:

HELOC Option:

- Amount: $100,000

- Rate: 7.50% (variable)

- Draw Period: 10 years (interest-only payments)

- Repayment Period: 20 years

- Monthly Payment (draw period): $625 (interest only)

- Monthly Payment (repayment): $807 (principal + interest)

- Closing Costs: Approximately $2,000

- First 10 Years Total Cost: $75,000 (interest only)

Home Equity Loan Option:

- Amount: $100,000

- Rate: 7.00% (fixed)

- Term: 20 years

- Monthly Payment: $775 (principal + interest)

- Closing Costs: Approximately $2,500

- First 10 Years Total Cost: $93,000 (principal + interest)

Cash-Out Refinance Option:

- New Mortgage Amount: $300,000 ($200,000 + $100,000)

- Rate: 6.50% (assuming currently favorable rate)

- Term: 30 years

- Monthly Payment: $1,896 (principal + interest on entire amount)

- Closing Costs: Approximately $6,000

- First 10 Years Total Cost: $227,520 (for entire mortgage)

Decision Framework

Consider these factors when choosing between equity options:

- Current Mortgage Rate: If your existing rate is lower than current rates, a HELOC or home equity loan preserves that advantage.

- Timeline for Funds: Need all funds at once? Get a home equity loan. Need funds over time? A HELOC offers flexibility.

- Payment Preference: Want consistent payments? Choose a home equity loan. Comfortable with potential rate changes? A HELOC might work.

- Long-term Plans: Planning to sell in a few years? A HELOC’s lower initial costs might be beneficial.

South Texas Lending offers personalized consultation to help you determine which option best fits your specific financial situation and goals.

Using Your HELOC Funds Wisely

A HELOC can be a powerful financial tool when used responsibly. Here are some ways you can use your HELOC funds:

Home Improvements and Renovations

Invest in your home to increase its value while improving your quality of life. Popular projects include:

- kitchen or bathroom remodels

- room additions

- energy-efficiency upgrades

- major repairs and maintenance

Debt Consolidation

Using a HELOC to pay off high-interest debt can save money and simplify your finances. Consider consolidating:

- credit card balances

- personal loans

- auto loans

- other high-interest debts

Education Expenses

HELOCs often offer lower interest rates than student loans and can be used for:

- college tuition and fees

- graduate school expenses

- educational materials and equipment

- on-campus housing costs

Emergency Fund

Use a HELOC as a financial safety net for unexpected expenses like:

- medical emergencies

- essential home repairs

- temporary income loss

- major car repairs

Investment Opportunities

Some homeowners use HELOCs to fund investments like:

- business ventures

- real estate purchases

- stock market investments

- retirement accounts

Important Note: A HELOC uses your home as collateral, which means you could lose it if you can’t repay what you borrow. Always speak with a financial advisor before using your home’s equity for investments.

Current HELOC Rates in Texas

HELOC rates in Texas tend to follow national trends, but your specific rate will depend on your credit profile, loan amount, and property value. As of May 2026, South Texas Lending is offering competitive rates starting at:

Current STX Lending HELOC Rates

| Credit Score | Rate (APR) | Features |

|---|---|---|

| 740+ | 7.25% | Best rates, highest credit limits |

| 700-739 | 7.75% | Excellent rates, flexible terms |

| 660-699 | 8.50% | Good rates, standard terms |

| 620-659 | 9.25% | Higher rates, may have additional requirements |

7Rates are variable and based on Prime Rate + margin. Rates shown include 0.25% discount for autopay from an STX checking account.

HELOC Rate Trends (2025-2026)

Heading into 2026, national HELOC averages remain elevated relative to historical norms. High-7% range is typical, though specific quotes shift with Fed policy.

Rates began trending down after the Federal Reserve initiated rate cuts in late 2024, and that easing carried into 2025-2026. Pace and final destination depend on Fed policy decisions, but the broader environment is more borrower-friendly than it was 18 months ago.

For Texas homeowners, this could be a great time to secure a HELOC. After the previous years’ high interest rates, rates are finally trending downward. South Texas Lending consistently offers rates lower than the national average for qualified borrowers.

What Affects Your HELOC Rate

Several factors play a role in the interest rate you’ll receive on your HELOC:

- Credit Score: The higher your score, the better the rate you’re likely to get

- Loan-to-Value Ratio: Lower LTVs typically receive better rates

- Relationship Discounts: If you already have accounts with South Texas Lending, you could qualify for a rate discount

- Property Type: Single-family homes usually qualify for better rates than condos

- Loan Amount: Some lenders offer better rates for larger credit lines

- Economic Conditions: Fed rate decisions directly impact variable HELOC rates

Why Choose STX Lending?

South Texas Lending offers several rate advantages over many other Texas HELOC lenders:

- HELOC amounts from $20,000 up to $500,000

- no application fees or annual maintenance fees

- rate discounts for existing customers (up to 0.50% off)

- no closing costs on lines of $250,000 or less

- option to lock in your rate during the draw period

- ability to convert to a fixed rate after the draw period ends

Tax Implications of Texas HELOCs

Understanding the tax implications of a HELOC is essential for maximizing potential benefits while remaining compliant with current tax laws.

Tax Deductibility of HELOC Interest

The Tax Cuts and Jobs Act of 2017 modified the rules for deducting HELOC interest:

- Deduction Limitations: HELOC interest is only deductible when the funds are used to “buy, build, or substantially improve” the home securing the loan

- TCJA Provisions: Original TCJA mortgage-interest deduction rules ran through the 2025 tax year. Confirm current rules with your tax professional

- Deduction Cap: Total mortgage debt eligible for the interest deduction is limited to $750,000 ($375,000 if married filing separately)

What Qualifies as “Substantially Improving” Your Home?

Examples of qualifying home improvements include:

- kitchen or bathroom remodels

- room additions

- roof replacement

- HVAC system upgrades

- major structural repairs

Non-Deductible Uses

HELOC interest is not tax-deductible when used for:

- debt consolidation

- education expenses

- medical bills

- vacations or personal expenses

- investment opportunities unrelated to your home

Documentation Requirements

To claim the deduction, you should maintain:

- records of all home improvement expenses

- receipts for materials and contractor payments

- before and after photos of improvements

- home improvement contracts

Always consult with a qualified tax professional before claiming HELOC interest deductions on your tax return.

Potential Pitfalls and How to Avoid Them

HELOCs can be incredibly useful. But like any financial tool, they come with risks. Knowing what to watch for helps you use them wisely and stay on track.

Payment Shock After Draw Period

The Challenge: When the interest-only draw period ends, monthly payments can increase significantly as you begin paying both principal and interest.

Solution: Be ready for higher payments by:

- making principal payments during the draw period

- setting aside extra cash now for future payment increases

- looking into refinancing options before the draw period ends

Variable Interest Rate Risk

The Challenge: Most HELOCs have variable interest rates that can increase. If rates go up, your payments do too.

Solution: Protect yourself by:

- budgeting for potential rate hikes

- choosing HELOC products with rate caps

- switching to a fixed rate when rates are low

Overuse of Available Credit

The Challenge: Easy access to funds may lead to borrowing more than necessary.

Solution: Borrow smart by:

- creating a specific plan for HELOC funds before borrowing

- only drawing what you need, when you need it

- setting personal limits lower than your maximum credit line

Property Value Fluctuations

The Challenge: If home values decline, this could leave you owing more than your home is worth.

Solution: Limit this risk by:

- borrowing conservatively (below maximum limits)

- keeping an eye on local real estate trends

- making extra principal payments when you can

Foreclosure Risk

The Challenge: Since your home secures the HELOC, defaulting puts your home at risk of foreclosure.

Solution: Protect your home by:

- ensuring you can afford payments even if financial situations change

- building an emergency fund for backup

- contacting your lender immediately if you run into financial trouble

Real-World Examples: Texas HELOC Success Stories

These real-life scenarios (with names changed) show how Texas homeowners used HELOCs to reach their financial goals.

Case Study 1: The Home Improvers

Homeowners: Michael and Sarah, Austin Home Value: $450,000 Existing Mortgage: $250,000 HELOC Amount: $110,000 Project: Complete kitchen and master bathroom renovation

Their Experience: Michael and Sarah wanted to update their 25-year-old kitchen and bathroom without wiping out their savings. They got a $110,000 HELOC (staying within the 80% combined LTV limit) and withdrew funds in stages as their renovation progressed.

During the 14-month remodel, they made interest-only payments. When the renovations were done, they started paying down the principal. The improvements boosted their home’s value by about $85,000.

Key Takeaway: Using a HELOC for home improvements allowed them to enhance their living space and increase their property value without liquidating investments or depleting emergency savings.

Case Study 2: The Debt Consolidator

Homeowner: Carlos, San Antonio Home Value: $320,000 Existing Mortgage: $140,000 HELOC Amount: $50,000 Project: Consolidate high-interest credit card debt

His Experience: Carlos had built up $48,000 in credit card debt at an average interest rate of 22%. He obtained a HELOC at 7.75%, paid off all his credit card debt, and slashed his monthly interest payments by over $550.

Carlos committed to a five-year repayment plan, making consistent monthly payments well above the minimum required. He also cut up most of his credit cards to avoid accumulating new debt.

Key Takeaway: A HELOC provided significant interest savings and a structured path to becoming debt-free, but required financial discipline to avoid rebuilding credit card debt. A debt consolidation refinance can be an alternative if you’d rather roll the balances into a new first lien.

Case Study 3: The Education Funder

Homeowners: Jennifer and David, Houston Home Value: $380,000 Existing Mortgage: $180,000 HELOC Amount: $80,000 Project: Fund their children’s college education

Their Experience: With twins heading to college, Jennifer and David needed more than their college savings could offer. They obtained an $80,000 HELOC and pulled money out each semester as needed.

Compared to private student loans, the HELOC’s lower rate saved them around $12,000 in interest over four years. They also appreciated the flexibility to draw only what they needed each semester rather than borrowing a lump sum upfront.

Key Takeaway: A HELOC provided lower interest rates than education-specific loans while offering the flexibility to borrow only what was needed when it was needed.

Compare South Texas Lending to Other Texas HELOC Lenders

To help you make an informed decision, here’s how South Texas Lending compares to other major HELOC providers in Texas:

| Feature | South Texas Lending | Major Bank Lenders | Credit Unions | Online Lenders | |

|---|---|---|---|---|---|

| Starting APR | 7.25% | 7.75-8.50% | 7.50-8.25% | 7.99-9.50% | |

| Min. Credit Score | 620 | 660-680 | 640-660 | 620-680 | |

| Max LTV | 80% | 70-80% | 80% | 80-90% | |

| Line Amounts | $20K-$500K | $25K-$1M | $10K-$250K | $15K-$400K | |

| Annual Fees | None | $50-$75 | $0-$50 | None | |

| Closing Costs | 0-2% | 1-3% | 0-2% | 0-4.99% | |

| Draw Period | 10 years | 5-10 years | 5-15 years | 5-10 years | |

| Repayment Period | 20 years | 10-20 years | 10-20 years | 15-30 years | |

| Fixed-Rate Option | Yes | Sometimes | Rarely | Sometimes | |

| Processing Time | 30-35 days | 45-60 days | 30-45 days | 14-45 days | |

| Special Features | Rate discounts, closing cost credits | Branch access, relationship discounts | Member-only rates, personalized service | Fast online applications, digital dashboard |

Frequently Asked Questions

Can I get a HELOC on an investment property in Texas?

No. Texas law only allows home equity lines of credit (HELOCs) on your primary home (called a homestead). That means you can’t get a HELOC for a rental, vacation home, or any investment property.

How long does it take to get approved for a HELOC in Texas?

The process usually takes about 30 to 45 days. Texas has a 12-day waiting period between application and closing.

What is the minimum credit score needed for a HELOC in Texas?

Most lenders, including South Texas Lending, look for a credit score of at least 620. If your score is over 700, you may qualify for better interest rates.

Can I have both a HELOC and a home equity loan in Texas?

No. Texas law allows just one home equity loan type at a time. You’d need to pay off the current one before getting another.

Are HELOC interest payments tax-deductible?

They might be, but only if you use the funds to buy, build, or significantly improve the home tied to the loan. These deductions ran through the 2025 tax year under TCJA; current treatment may differ. Check with a tax expert for advice based on your situation.

Can I pay off my Texas HELOC early?

Yes! With South Texas Lending, there are no prepayment penalties. You can pay off your HELOC whenever you want without any extra fees.

What happens when my draw period ends?

Once your draw period ends (usually after 10 years), you won’t be able to borrow more money. At that point, you start repaying both the principal and interest until the full amount is paid off.

HELOC Decision Tool: Is It Right for You?

Not sure if a HELOC fits your needs? This simple flowchart can help you figure out if a Texas HELOC is a good financial option for your situation.

HELOC Suitability Questionnaire

Answer these questions to see if a HELOC could work for you:

- Do you have at least 20% equity in your primary residence in Texas?

- Yes: Continue to question 2

- No: A HELOC may not be available to you at this time

- Is your credit score 620 or higher?

- Yes: Continue to question 3

- No: You may need to improve your credit before applying

- Is your debt-to-income ratio below 43%?

- Yes: Continue to question 4

- No: You may need to reduce existing debt first

- Are you planning to use the funds for a specific purpose with a clear repayment plan?

- Yes: Continue to question 5

- No: Consider creating a more defined financial plan before proceeding

- Are you comfortable with potential payment increases if interest rates rise?

- Yes: Continue to question 6

- No: Consider a fixed-rate home equity loan instead

- Do you expect to stay in your home for at least 3-5 years?

- Yes: A HELOC may be suitable for your needs

- No: Consider other financing options with fewer upfront costs

HELOC Calculator

Want to estimate how much you might qualify for with a South Texas Lending HELOC? Use our calculator.

Home Value Calculator

Home Value: $__________ Current Mortgage Balance: $__________ Other Liens (if any): $__________ Credit Score: [Dropdown: 620-659, 660-699, 700-739, 740+]

Click Calculate to see your potential HELOC amount, estimated rate, and monthly payments

Complete HELOC Application Checklist

Get ready for your HELOC application by gathering these documents:

Personal Information

- ☐ Valid government-issued photo ID

- ☐ Social Security number

- ☐ Current contact information

- ☐ Marital status documentation (if applicable)

Property Documentation

- ☐ Current mortgage statement

- ☐ Homeowners insurance policy

- ☐ Property tax statements (most recent)

- ☐ HOA information (if applicable)

- ☐ Deed or title information

Income Verification

- ☐ Pay stubs (last 30 days)

- ☐ W-2 forms (last 2 years)

- ☐ Federal tax returns (last 2 years)

- ☐ 1099 forms (if self-employed or have additional income)

- ☐ Retirement/pension documentation (if applicable)

- ☐ Alimony/child support documentation (if applicable)

Financial Information

- ☐ Bank statements (last 2-3 months)

- ☐ Investment account statements

- ☐ Retirement account statements

- ☐ List of all debts and obligations

- ☐ Explanation of any recent credit inquiries

- ☐ Bankruptcy discharge papers (if applicable)

For Self-Employed Applicants

- ☐ Business tax returns (last 2 years)

- ☐ Profit and loss statements (current year)

- ☐ Business bank statements (last 2-3 months)

- ☐ Business license or similar documentation

Additional Documents (if applicable)

- ☐ Trust documentation (if property is held in a trust)

- ☐ Power of attorney documentation

- ☐ Divorce decree or separation agreement

- ☐ Gift letters (if using gift funds)

Pro Tip: Organize all documents digitally before beginning your application. South Texas Lending offers a secure document upload system to streamline the process.

Glossary of HELOC Terms

Here are some key terms to know as you go through the HELOC process.

Advance: The act of borrowing money against your HELOC.

Annual Percentage Rate (APR): The yearly cost of borrowing money, expressed as a percentage, including interest and certain fees.

Combined Loan-to-Value Ratio (CLTV): The ratio of all secured loans on a property to the property’s appraised value.

Draw Period: The timeframe (typically 10 years) during which you can borrow from your HELOC.

Equity: The difference between your home’s market value and the amount you owe on your mortgage(s).

Homestead Property: In Texas, your primary residence that receives certain legal protections.

Index Rate: The base interest rate (usually the Prime Rate) to which the margin is added to determine your HELOC interest rate.

Interest-Only Payments: Payments that cover only the interest charged, not the principal balance.

Lien: A legal claim against a property that serves as security for a debt.

Margin: The percentage points added to the index rate to determine your HELOC interest rate.

Principal: The amount of money borrowed or still owed on a loan, separate from interest.

Rate Cap: A limit on how much your interest rate can increase during a specified period.

Repayment Period: The phase following the draw period when you can no longer borrow funds and must repay the outstanding balance.

Right of Rescission: The legal right to cancel a home equity loan or HELOC within three business days after closing.

Variable Rate: An interest rate that fluctuates based on changes to the underlying index rate.

Ready to Unlock Your Home’s Equity?

We’re here to guide you through every step. Whether you prefer to apply online, by phone, or in person, we’ve made it easy to get started.

Get Started Today:

- Online: Fill out our secure application

- By Phone: Call us at 210-750-6461

Check Your Rate: Use our HELOC calculator to estimate your potential HELOC rate and amount without affecting your credit score, and compare a home equity loan vs HELOC if you’re still deciding.

Every borrower's situation is unique. The guidelines above are general — speak with a licensed loan officer to understand how they apply to you specifically.

Ready to Get Started?

STX Lending is a Texas-owned direct lender with decades of combined experience. Whether you're buying your first home or refinancing for better terms, our team is here to help.

Ready to take the next step on your home loan?

Apply online for expert-recommended options customized to your budget.

Start my application