Looking at your mortgage balance and then seeing your 401k savings might give you an idea:

“What if I just use my 401k to pay off my house?”

It’s a tempting thought but is it actually a smart financial move? The answer depends on your unique situation. You should factor in your financial goals, retirement timeline, and tax status.

This guide will walk you through everything you need to consider before making a big decision. We’ll go over taxable income, hardship withdrawal, paying off with fixed income, and more.

Key Points

- Using 401k savings to pay off a mortgage will trigger taxes that could enable you to pay taxes as an early withdrawal fee.

- A $100,000 withdrawal could shrink your retirement savings, meaning you could lose long-term financial security.

- With interest rates in 2025 being over 6%, and 401k market returns averaging 7%, the compound interest could have you keep funds in your 401k.

- For most people under 59, using 401k funds to pay off a mortgage just doesn’t make financial sense.

Understanding Your Options: 401 K Loans vs. Withdrawals

There are two main ways to access your 401k for a mortgage payoff:

401 k Loans

With a 401k loan, you’re essentially borrowing from yourself. You can typically take up to 50% of your balance or $50,000, whichever is less. You’ll pay it back, with interest, over about five years.

The good stuff: No immediate tax hit. The interest you pay goes back into your retirement account. And if you miss payments, it won’t trash your credit score.

What’s the catch?

Most people can’t borrow enough to pay off a mortgage entirely. And if you leave your job (voluntarily or not), that loan typically becomes due within 60-90 days. If you can’t pay it back in that window, it converts to a withdrawal, which means…

Direct Withdrawals

This is where you simply take money out of your 401k. No payback required

The upside is obvious: You can potentially get enough cash to eliminate your mortgage in one fell swoop. But the costs are steep — especially if you’re under 59½.

You’ll pay ordinary income tax on the entire withdrawal. Plus, if you’re under 59½, expect a 10% early withdrawal penalty. And since the money is gone from your retirement account, you also lose that money’s ability to grow in the market — forever.

The Real Cost: Breaking Down the Numbers

Let’s say you’re 45 years old, have a $200,000 mortgage, and want to pay it off using your 401k.

Here’s a rough estimate of what you’ll actually end up with:

- Federal tax withholding (20%): $40,000

- Early withdrawal penalty (10%): $20,000

- Possible additional federal taxes (depending on your tax bracket): $8,000

- State taxes (varies by state): $5,000-$16,000

So, from your $200,000 withdrawal, you might only get $120,000 to $130,000 after taxes and penalties. That’s a major hit.

But wait, there’s more. The biggest cost might be what you don’t see: the lost growth.

If that $200,000 had stayed invested earning a modest 7% annual return:

- In 10 years, it would grow to around $393,000

- In 20 years, it would reach about $774,000

- In 30 years, it would balloon to over $1.5 million

As James, a financial advisor I spoke with while researching this article, put it:

“People focus on the immediate tax hit, which is bad enough. But the real cost is what that money could have become by retirement age. It’s like cutting down an apple tree for one season’s worth of apples.”

When It Might Make Sense to Use Your 401k

There are rare situations where using your 401(k) to pay off your home could work:

High Mortgage Rate: If you’re paying 6.5% or more on your mortgage and conservative investment options are yielding much less, the guaranteed “return” from eliminating high-interest debt might outweigh the potential investment returns — especially if you’re nearing retirement.

Substantial retirment Savings: If your 401k is just one part of a diverse retirement strategy that includes other accounts, pensions, or significant assets, using a portion of your 401k might not jeopardize your long-term security.

When Not To Dip into your 401-k

For most people, especially those under 59½, here’s when it’s better to leave your 401k alone:

The younger you are, the more valuable your retirement savings become – thanks to compound growth. Using those funds early means missing out on decades of potential gains.

Consider Michael, who at 42 was tempted to use $250,000 from his $320,000 401(k) to pay off his mortgage. After running the numbers with a financial advisor, he decided against it. Instead, he increased his monthly mortgage payment by $400. Ten years later, his 401k had grown to nearly $780,000, and his additional payments had cut his mortgage term by a decade, saving him $120,000 in interest. “I’m glad I didn’t raid my retirement,” he says. “I’m getting the best of both worlds.”

Limited Retirement Savings: If your 401k is your main (or only) source of retirement money, don’t touch it.

High Revolving , high interest Debt: Credit cards, personal loans, or auto loans typically carry much higher interest rates than mortgages. Pay those down first.

Low Mortgage Interest Rate: If you locked in a 3-4% rate, your 401k likely earns more over time. Keep the loan and let your retirement savings grow.

Real People, Real Decisions: Case Studies

Case Study 1: Pre-Retirement Couple (Ages 58 and 59)

Situation:

- 401k balance: $950,000

- Mortgage balance: $180,000 at 6.2% interest (12 years remaining)

- Monthly payment: $2,100

- Other retirement assets: $350,000 in IRAs and $100,000 in taxable investments

Decision: They used $200,000 from their 401(k) to pay off their mortgage at age 59½, avoiding early withdrawal penalties.

Outcome:

- Eliminated $2,100 monthly payment

- Paid approximately $50,000 in federal and state taxes on the withdrawal

- Reduced monthly expenses significantly before retirement

- Still maintained adequate retirement savings

- Reported improved peace of mind and ability to retire 2 years earlier than planned

Case Study 2: Mid-Career Professional (Age 42)

Situation:

- 401k balance: $320,000

- Mortgage balance: $250,000 at 4.8% interest (25 years remaining)

- Monthly payment: $1,425

- Other assets: $50,000 emergency fund, minimal other investments

Decision: After calculating the costs, he decided NOT to use 401k funds and instead increased his regular monthly payment by $400.

Outcome:

- Will pay off mortgage 10 years early, saving $120,000 in interest

- 401k continued to grow, reaching $780,000 by age 52

- Maintained tax advantages of mortgage interest deduction during peak earning years

- Built additional equity through housing market appreciation

Better Alternatives to Consider to Pay Off a Mortgage

Before tapping your 401k, explore these often-overlooked options:

Refinancing

Current mortgage rates in 2025 average 5.3% for a 30-year fixed and 4.8% for a 15-year fixed. If your rate is higher, refinancing could save you thousands.

For example, refinancing a $300,000 mortgage from 6.5% (30-year) to 4.8% (15-year):

- increases your monthly payment from $1,896 to $2,338 (+$442/month)

- saves approximately $182,000 in total interest

- pays off your mortgage 15 years sooner

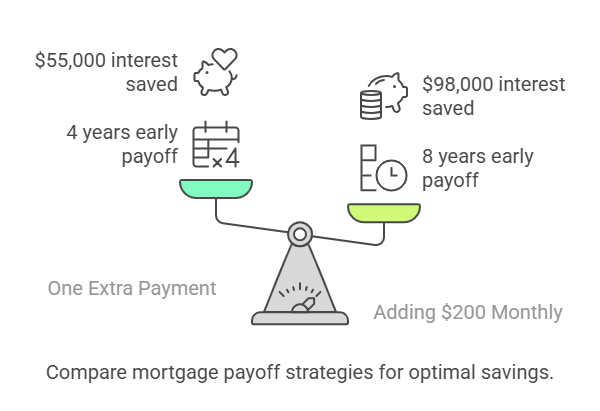

Making Extra Mortgage Payments

Instead of a lump-sum payoff, consider these strategies:

- One extra payment yearly: Pays off a 30-year mortgage about 4 years early, saving around $55,000 in interest on a $300,000 loan at 5.3%

- Adding $200 extra monthly: Cuts about 8 years off the same mortgage, saving nearly $98,000 in interest

- Biweekly payments: Essentially makes one extra payment per year, cutting about 4 years off your mortgage

Sarah, a teacher in Texas, couldn’t afford an extra full payment each month. Instead, she rounded her $1,450 payment up to $1,700. “It didn’t feel like a huge sacrifice month-to-month, but it’s taking almost 7 years off my mortgage,” she says.

Downsizing

If reducing housing costs is your primary goal, consider selling your current home and buying a less expensive one outright or with a much smaller mortgage.

A couple in California sold their $650,000 home with $350,000 in equity, purchased a $300,000 condo outright, and still had $50,000 left to boost their retirement savings—all without touching their 401(k).

Focus on Other Debt First

If you have credit cards charging 18-24% interest or personal loans at 10%+, tackle these first. The interest savings will be far greater than paying off a mortgage at 4-6%.

Detailed Calculations: What the Numbers Really Show

Let’s compare three approaches for someone with a $200,000 mortgage balance at 5.3% with 20 years remaining:

Option 1: Continue Regular Payments

- Monthly payment: $1,349

- Total remaining payments: $323,760

- Total remaining interest: $123,760

Option 2: 401(k) Withdrawal to Pay Off Mortgage

- Withdrawal needed (age 50): $266,000 (to cover taxes and penalties)

- Immediate tax cost: $66,000

- Lost growth over 15 years (at 7%): $460,000

- Interest saved: $123,760

- Net financial impact: -$402,240

Option 3: Add $500/month to Mortgage Payment

- New monthly payment: $1,849

- Payoff time: 11.5 years (8.5 years sooner)

- Total payments: $255,162

- Interest saved: $68,598

- Growth of $500/month invested for 8.5 years after mortgage payoff: $73,000

- Net financial impact: +$141,598

The numbers don’t lie — Option 3 wins by a landslide for most scenarios.

Common Questions, Quick Answers

“Can I use my 401k funds penalty-free to pay off my mortgage?”

Only if you’re 59½ years old or older. There’s no mortgage exception to avoid the 10% penalty before that age.

“What happens if I take a 401k loan and then leave my job?”

You’ll likely have 60-90 days to repay the entire loan. If you can’t, the loan converts to a withdrawal, subject to taxes and potentially that 10% early withdrawal penalty.

“How will paying off my mortgage affect my taxes?”

You’ll lose the mortgage interest deduction if you itemize. However, with the standard deduction at $14,600 for single filers and $29,200 for married filing jointly in 2025, many homeowners don’t itemize anyway.

“Can I use a Roth 401k instead?”

Yes. Qualified withdrawals from a Roth 401k (if you’re over 59½ and the account is at least 5 years old) would be tax-free, which improves the math. However, early withdrawals of earnings are still taxable and penalized.

“How much will this decision hurt my retirement income?”

As a general rule, every $100,000 withdrawn from a retirement account at age 55 could reduce your potential monthly retirement income by approximately $500-$650 at age 65, assuming average market returns.

Before You Decide: Essential Checklist

Make sure you gather the following:

✓ Your Numbers

- Current 401(k) balance and investment allocation

- Current mortgage balance, interest rate, and remaining term

- Latest tax return to assess your tax situation

- Retirement income projections

- Current and projected monthly expenses

✓ Professional Input

- Financial advisor to analyze impact on retirement planning

- Tax professional to calculate specific tax implications

- Mortgage lender to explore refinancing options

Making the Right Choice for Your Situation

At the end of the day, this decision isn’t purely mathematical. Your comfort with debt, proximity to retirement, and overall financial situation all play important roles.

For some people, the peace of mind from being mortgage-free outweighs the financial costs. For others, keeping retirement funds intact provides greater long-term security.

What’s most important is making an informed decision based on your complete financial picture—not just eliminating a monthly payment.

Next Steps: Get Personalized Guidance

If you’re seriously considering using retirement funds to pay off your mortgage, your next step should be getting professional guidance specific to your situation.

At South Texas Lending, we offer a specialized retirement-mortgage analysis designed for homeowners weighing this exact decision. Our analysis includes:

- A detailed tax impact calculation based on your specific situation

- Side-by-side comparison of all available options

- Custom mortgage payoff strategies tailored to your financial goals

- Refinancing alternatives that might accomplish your goals without touching retirement funds

Whether you ultimately decide to use retirement funds or explore alternatives, having a clear understanding of the implications will help you make the choice that’s right for your financial future.

Ready to explore your options? Contact STX Lending today for your complimentary Retirement-Mortgage Analysis and take the next step toward financial clarity.