As an investor in Texas, you might assume you’re set to get approved for a traditional loan. But then, your tax returns reveal that your income is lower than expected. What now? Here’s where DSCR loans (Debt Service Coverage Ratio loans) come in. Instead of focusing on your personal income, DSCR loans look at the

Introduction

As an investor in Texas, you might assume you’re set to get approved for a traditional loan. But then, your tax returns reveal that your income is lower than expected. What now?

Here’s where DSCR loans (Debt Service Coverage Ratio loans) come in. Instead of focusing on your personal income, DSCR loans look at the potential income your investment property generates. This makes them an attractive option for real estate investors, especially in Texas.

Let’s break it down.

Key Takeaways

- DSCR loans allow investors to qualify using rental income from their properties, not their personal income or tax returns.

- Requirements include a minimum 620-660 credit score, a 20-25% down payment, and at least 1.0 DSCR ratio.

- Current interest rates for DSCR mortgage loans in Texas start around 5.99%, with loan amounts available up to $3.5 million.

- You can use Texas DSCR loans for investment properties, including single-family homes, multi-family units, and short-term rentals.

- Check your DSCR loan eligibility with South Texas Lending today

What is a DSCR Loan?

A DSCR loan (Debt Service Coverage Ratio loan) is a type of mortgage where lenders focus on the property’s ability to pay for itself through rental income, rather than looking at your personal financials, like W-2s or tax returns.

Simply put, it’s almost as if the property is applying for the loan on its own, and you’re just the co-signer.

The Debt Service Coverage Ratio (DSCR) is a key metric used to assess this. It compares the income the property generates to the costs it takes to keep it running, including the mortgage payment. To calculate it, you divide the property’s income by its total expenses.

The result is pretty straightforward.

A DSCR above 1 means the property is earning enough to cover its expenses, plus some extra cash flow. A DSCR below 1, on the other hand, means the property isn’t generating enough to cover its costs, so you’d have to make up the difference out of pocket.

Here’s a quick example:

Your rental property brings in $2,000 monthly, and the total monthly cost (mortgage, taxes, insurance) runs $1,600. Doing the math: 2000 ÷ 1600 = 1.25. That 1.25 DSCR tells lenders the property earns 25% more than it needs to cover its costs.

How Do DSCR Loans Work in Texas?

Texas DSCR loans are designed with investors in mind, especially those who might not fit the mold for traditional mortgages.

With DSCR loans, lenders care more about the income your property brings in than your personal income or tax returns. This makes the process much simpler, especially for self-employed investors or those with complex financial situations.

DSCR loans in Texas are strictly for investment properties. Not homes you plan to live in. That includes:

- long-term rental homes

- short-term vacation rentals (like Airbnb)

- multi-family buildings

You can take out a DSCR loan as an individual, or through an LLC or corporation, giving you more flexibility in how you structure your investments.

Traditional loans often limit you to 10 financed properties. DSCR loans, on the other hand, let you finance as many properties as you want. As long as each one meets the lender’s DSCR requirements. That makes it easier to grow your portfolio over time.

How DSCR Loans Differ from Conventional Loans

| Feature | DSCR Mortgage Loans | Conventional Loans |

|---|---|---|

| Qualification Basis | Property’s rental income | Borrower’s personal income |

| Documentation | Minimal (no tax returns/W2s) | Extensive income documentation |

| Property Use | Investment properties only | Primary residences, second homes, investments |

| Minimum Down Payment | 20-25% typically | As low as 3% for primary residences |

| Property Limit | No set limit | Maximum 10 financed properties |

| Entity Options | Individual, LLC, Corp | Typically individual borrowers only |

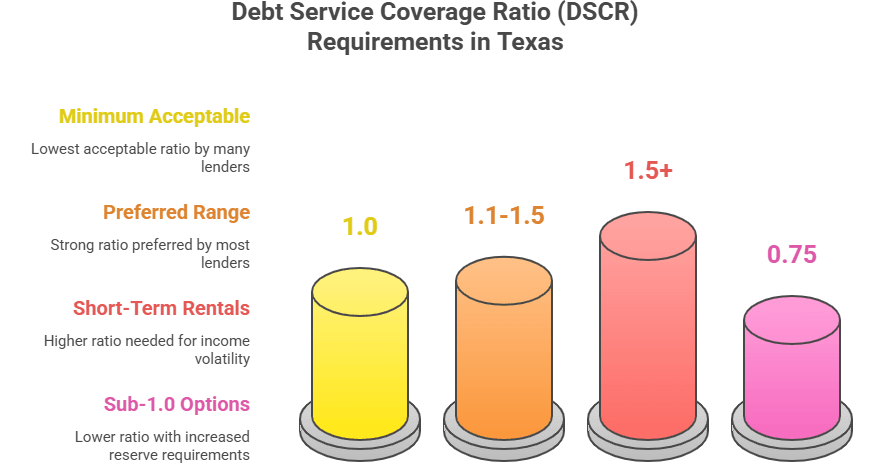

Texas DSCR Loan Requirements

Here’s a breakdown of the requirements and factors that can affect your loan approval process.

Minimum Credit Score Requirements

Most Texas DSCR lenders want to see at least 620 on your credit report, but that just gets you in the door. I’ve seen firsthand how borrowers with that minimum credit score get stuck with higher rates and stricter terms. Push your score into the 700+ territory if you can – that’s when the good stuff happens: better rates, higher loan-to-value ratios, and fewer hoops to jump through.

Minimum Down Payment Requirements

Most DSCR loans want 20-25% down, which can be a tough pill to swallow if you’re used to those 3% down conventional options. The experience factor matters too – if you’ve already got rental properties in your portfolio, you might qualify for 20% down, while first-timers often get stuck putting down 25%. The property’s performance also influences this – a borderline DSCR ratio might force you into 25-30% down territory.

DSCR Ratio Requirements

Most lenders require a minimum DSCR of 1.0 to 1.2, meaning the property must generate enough rental income to at least cover its debt obligations. This coverage ratio dscr loan is crucial in evaluating the financial viability of investment properties. Higher ratios (1.25+) typically result in better loan terms and lower interest rates.

Property Types Eligible for DSCR Loans

Eligible properties include:

- Single-family residences

- 2-4 unit multi-family properties

- Condominiums and townhomes

- Short-term vacation rentals (Airbnb/VRBO)

- Small apartment buildings (some lenders)

The key requirement is that the subject property must be used for investment purposes and generate rental income.

Loan Limits and Cash Reserves

For investment property financing, DSCR loan amounts generally range from $100,000 up to $3,000,000, though some lenders offer up to $5,000,000 depending on the property’s DSCR ratio.

Cash reserve requirements are another important consideration:

- Standard Requirement: 6 months of debt payments for DSCR ≥ 1.0

- Lower DSCR Properties: 12 months reserves for DSCR < 1.0

Benefits of DSCR Loans for Real Estate Investors

If you’re an investor looking for more flexibility and less red tape, these DSCR loans are definitely worth considering.

No Income Verification

With DSCR loans, tax strategies won’t come back to haunt you. I’ve seen countless self-employed investors get rejected for traditional financing despite having substantial assets and cash flow. DSCR loans skip the whole pay stub and tax return hustle entirely. Your property’s income matters more than the borrower’s personal income – a game-changer for savvy investors who understand tax efficiency.

Portfolio Expansion

Traditional lenders start sweating when you hit 4-6 properties, and most slam the door after 10. DSCR mortgage loans don’t play by those rules. I’ve watched investors build impressive portfolios of multiple properties one DSCR loan at a time, without the typical debt-to-income roadblocks. The conventional financing ceiling doesn’t apply here, which means your ambition doesn’t need to have limits either.

Faster Approval Process

Nothing kills real estate deals faster than slow financing. While your competition is still gathering tax returns and employment verification for conventional loans, you could already have keys in hand with a DSCR loan. The typical closing timeline runs 2-4 weeks instead of the excruciating 45-60 day marathon of traditional mortgages.

Entity-Based Ownership

LLC ownership isn’t just fancy paperwork – it’s serious asset protection. Most traditional loans force you to hold property in your personal name, creating a direct liability connection to your personal assets. DSCR loans typically allow entity ownership, creating that crucial separation between your investment activities and your personal finances.

Short-Term Rental Flexibility

Try telling a conventional lender you plan to list your property on Airbnb – watch how quickly they show you the door. DSCR loans and rental loans generally embrace short-term rental strategies that can significantly boost your returns in tourist hotspots. The ability to pivot between long-term and short-term rental strategies gives investors tactical options that conventional financing simply doesn’t support.

DSCR Loan Calculator: Understanding the Formula

The math behind DSCR isn’t rocket science, but getting it right before you apply can save you tons of headaches. Using a DSCR loan calculator before you apply can help you determine if a property will meet lender requirements.

DSCR Formula:

DSCR = Total Annual Rental Income ÷ Annual Debt Service

For rental income, lenders usually pick the lower number between current leases and what an appraiser says the market rent should be. On the expense side, they total up principal, interest, property taxes, insurance, and HOA fees if applicable.

How to Calculate DSCR for Texas Rental Properties

For tenant-occupied properties, most lenders compare your current lease agreement against the appraiser’s opinion of market rent (Form 1007), then use whichever number is lower.

With vacant properties, you’re at the mercy of the appraiser’s market rent determination on Form 1007.

For short-term rentals, some lenders will consider your actual Airbnb/VRBO track record if you’ve got one, while others accept projections from services like AirDNA.

The property’s rental income is crucial in these evaluations as it directly impacts the Debt Service Coverage Ratio (DSCR) calculation, determining how well the income generated can cover the debt obligations.

DSCR Calculation Example

Let me walk through a real-world example:

- Monthly Rental Income: $2,500 (confirmed by appraiser)

- Monthly Mortgage Payment (P&I): $1,600

- Monthly Property Taxes: $300

- Monthly Insurance: $100

- Monthly HOA: $0

Here’s how we calculate the DSCR:

- Annual rental income: $2,500 × 12 = $30,000

- Annual property expenses: ($1,600 + $300 + $100) × 12 = $24,000

- DSCR = $30,000 ÷ $24,000 = 1.25

That 1.25 DSCR meant the property generated 25% more income than needed for all expenses – comfortably above the minimum DSCR of 1.0-1.2 required by most lenders.

Texas DSCR Loan Costs and Interest Rates

Interest Rate Factors

Interest rates for DSCR loans in Texas start around 5.99%, though they fluctuate with market conditions. Don’t expect the rock-bottom rates you see advertised for primary residences. Your specific rate depends on your credit score, the property’s DSCR ratio, down payment size, loan amount, and property type.

Loan Terms and Options

Most Texas DSCR mortgage lenders offer several options:

- 30-year fixed-rate terms (some lenders offer 40-year terms)

- 5/1, 7/1, or 10/1 adjustable-rate mortgage options

- Interest-only payment options (typically for the first 5-10 years)

Prepayment Penalties

Unlike conventional home loans, the majority of DSCR loans include prepayment penalties if you pay off the loan before a specified period (usually 3-5 years). Common structures include:

- 3-2-1 (3% in year 1, 2% in year 2, 1% in year 3)

- 5-4-3-2-1 (declining percentage over 5 years)

How to Apply for a DSCR Loan in Texas

Step 1: Check Your Eligibility

Before starting the loan application process, verify that you meet the basic requirements:

- Confirm your credit score meets minimum requirements (620+)

- Ensure you have sufficient funds for down payment (20-25%)

- Calculate potential properties’ DSCR ratios to confirm they’ll qualify

- Check that the property type is eligible for DSCR financing

Step 2: Gather Required Documentation

“Minimal documentation” doesn’t mean “no documentation.” You’ll need:

- Government ID

- Property details and purchase contract if buying

- LLC/corporation documents if applicable

- Proof of funds for down payment and reserves

- Lease agreement (if property is currently leased)

Step 3: Choose a DSCR Lender

Select a lender that offers competitive terms by comparing:

- Interest rates and loan terms

- Down payment requirements

- Minimum DSCR and credit score requirements

- Closing costs and prepayment penalties

South Texas Lending specializes in helping investors find competitive DSCR loan options tailored to their specific investment strategy.

Step 4: Submit Application and Close

The application process typically includes:

- Pre-qualification assessment

- Property appraisal

- Underwriting review

- Loan approval and closing

The DSCR loan application process is generally faster than traditional mortgages, with many lenders able to close within 2-4 weeks.

DSCR Loan FAQs

Can I get a DSCR loan with no down payment in Texas?

No, unfortunately, you can’t. Every reputable DSCR lender will require a down payment, usually in the range of 20-25%. If you see ads claiming “no down payment” for DSCR loans, they likely mean they don’t closely check where the down payment comes from (like gift funds, for example), not that you can skip the down payment entirely.

What’s the minimum credit score for a Texas DSCR loan?

While some lenders may approve loans with a score as low as 620, your terms will be much better if your score is around 660-680. If you’re aiming for the best rates and the highest Loan-to-Value (LTV), you’d want your score to be above 700. If your score is on the lower side, it might be worth improving it before applying for a loan.

Can DSCR loans be used for Airbnb properties?

Yes, you can use DSCR loans for short-term rentals like Airbnb! In fact, it’s one of the few loan types that allows for this. However, lenders tend to have stricter requirements for short-term rentals because of the income unpredictability. Many lenders will require a higher DSCR (1.5 or more) for these types of properties.

How many properties can I finance with DSCR loans?

There’s no official cap on how many properties you can finance with DSCR loans, unlike conventional loans that limit you to 10 properties. I’ve worked with clients financing 30+ properties with DSCR loans. Since each property is assessed on its own financials, DSCR loans are a great option for building larger portfolios without hitting a limit.

Every borrower's situation is unique. The guidelines above are general — speak with a licensed loan officer to understand how they apply to you specifically.

Ready to Get Started?

STX Lending is a Texas-owned direct lender with decades of combined experience. Whether you're buying your first home or refinancing for better terms, our team is here to help.

Ready to take the next step on your home loan?

Apply online for expert-recommended options customized to your budget.

Start my application