Suppose you’re serving in the military and looking to buy a home with your VA benefits. In that case, you’ll learn that the Statement of Service Letter is the only thing standing in the way of your loan acceptance.

Missing or incomplete service letters are among the top reasons VA loans get delayed.

At South Texas Lending, we’ve helped hundreds of active-duty service members get home loans. Many come to us frustrated about paperwork delays that could have been avoided with the right information at the start.

A Statement of Service Letters can be hard to understand. But don’t worry. This guide will explain what they are, who needs them, and how to get yours without the usual problems that military homebuyers face.

Want to skip ahead? Check your VA loan eligibility now or contact a loan specialist at 210-750-6461.

What is a Statement of Service Letter?

A Statement of Service Letter is used by active-duty military members, reservists, and National Guard personnel to verify employment. Unlike a DD-214 (which veterans use), this letter confirms your current military status and income – two pieces of information mortgage lenders must verify before approving your VA loan.

The letter becomes a critical part of your loan application because lenders need proof that you:

- are currently employed by the military

- meet minimum service requirements for VA loan eligibility

- have a stable, verifiable income

- are likely to maintain that income during the early years of your mortgage

We’ve seen many service members get caught in application limbo because they didn’t realize how important this document would be to their loan approval. Starting the process without it is like trying to build a house without a foundation.

Who Needs a Statement of Service Letter?

The criteria will depend on your current military status.

Need a Statement of Service Letter:

- Active-duty members from any military branch

- Current reservists

- National Guard members

- Coast Guard members

- Space Force personnel

Need a DD-214 instead:

- Veterans who are discharged from service

- Retired military personnel

Here’s something that often confuses people: if you’re leaving the military but haven’t received your DD-214 yet, you’ll still need a Statement of Service Letter. Many lenders are unaware of this exception.

That’s why it’s important to work with a military-focused lender like South Texas Lending to save you both time and money.

What Must Be Included in Your Letter

When tracking down your statement of service letter, a VA mortgage lender may need more info. The lender could be looking for the following details in your letter:

Personal Details:

- Your full name

- SSN (last four digits mi)

- Date of birth

- Current rank/pay grade

Service Information

- Military branch

- Original entry date

- Time in service calculation

- Current area your stationed in

- Active duty status confirmation

Authentication Elements:

- Military letterhead

- Commander’s signature (or authorized representative)

- Signatory’s contact information

- Recent date (within 30 days of application)

Not all of the above is required per se, but missing critical elements could cause a rejection from underwriting. In the past, there have been some delays in underwriting because a commanding officer didn’t put the correct identifying information.

How to Get Your Statement of Service Letter

Getting your letter requires planning. The process typically works like this:

- Approach your commanding officer, executive officer, or unit admin with your request.

- Check in your VA Portal. Sometimes your information may already be available or partially completed in your VA portal.

- Clearly explain it’s for a VA home loan, and be specific about what information needs to be included.

- Check back within 3-5 business days if you still haven’t received your letter.

- Before submitting it to your lender, double-check the letter to make sure it includes all required details.

The biggest mistake we see? Waiting too long. Request your letter at least 30 days before you plan to apply for pre-approval.

Commands get busy, people go on leave, and administrative backlogs happen. Giving yourself a buffer helps ensure your homebuying process isn’t delayed by missing paperwork.

Branch-Specific Considerations

Different military branches handle Statement of Service Letters differently. Here’s what you should know:

Army

Army service members should work through their S-1 personnel section or unit administrators who are familiar with these requests. Letters typically require a signature from the company commander or higher, depending on your unit’s policies.

Navy

Sailors can request their letter through their command’s admin department or personnel office. Naval letters generally require the signature of the commanding officer, executive officer, or command master chief.

Air Force

Airmen should contact their First Sergeant or Military Personnel Flight (MPF). Air Force typically allows squadron commanders or mission support group representatives to sign these letters.

Marine Corps

Marines can request their letter through their S-1 or administration section. These typically require signature from the company commander or battalion commander.

Coast Guard

Coast Guard members should work through their administrative office. Letters generally require signature from the commanding officer or executive officer.

National Guard & Reserves

Typically guard and reverse duty member have to include the following in their letters:

Current activation status

- Title 10 or Title 32 orders (if relevant)

- Typical working Hours

- Any deployments coming up

Your unit admin or readiness NCO is normally the best resource for getting this documentation correctly.

Texas Military Installation Resources

If you’re stationed at one of Texas’s military bases, these local resources can help with document procurement:

Depending on which base you’re stationed in within Texas, here are some local numbers to contact to help you obtain your Service letter in Texas.

Joint Base San Antonio

The Housing Office provides document assistance on weekdays from 0800-1630. Contact: (210) 555-7890.

Fort Hood

Army Community Service offers VA loan document help. Contact: (254) 555-4321.

Naval Air Station Corpus Christi

Housing Office assists with VA loan documentation. Contact: (361) 555-8765.

Dyess Air Force Base

Airman & Family Readiness Center provides VA loan guidance. Contact: (325) 555-6543.

Other Ways to Get Your Statement of Service Letter

Getting a Statement of Service Letter isn’t always easy. If you’re running into issues, here are a few other ways to get the documentation you need:

Unit Adjutant or Personnel Office

If your commanding officer isn’t available, try your personnel office or unit adjutant. They often have access to your records and can usually issue the letter.

Digital Verification Tools

Some military branches now offer digital service verification. In certain cases, the “Status Report Pursuant to the Servicemembers Civil Relief Act” can also be used in place of a Statement of Service Letter. Just check with your lender first.

Installation Housing Office

Your base housing office often works directly with lenders and may even have templates ready that meet VA loan requirements.

What South Texas Lending Offers Military Members

At STX Lending, we’ve designed our VA loan process with active-duty service members in mind. Here’s what sets us apart:

- Help With Documents: We’ll guide you on exactly what your Statement of Service Letter needs to include.

- Military-Knowledgeable Staff: Our team includes veterans who truly understand military paperwork.

- Texas Installation Experts: Our loan officers know the ins and outs of bases like Lackland, Fort Sam Houston, and others across Texas.

- Evening & Weekend Support: We offer flexible appointment times that work with your duty schedule.

- PCS & Deployment Solutions: We’ve got special options for service members on the move or deployed overseas.

While other lenders may offer VA loans, few understand the unique challenges active-duty members face. On average, our military clients close 11 days faster than those using big banks — and often get a better rate, too.

Frequently Asked Questions

How recent does my Statement of Service Letter need to be?

Most lenders want it to be dated within 30 days of your loan application. If the process takes longer, you may need to provide an updated version before closing.

Can my executive officer or first sergeant sign instead of my commander?

Yes. Most lenders will accept signatures from your executive officer, first sergeant, adjutant, or personnel officer as long as they’re authorized to confirm your service details.

What if I’m currently deployed?

If deployed, work through your rear detachment commander or unit administration. Many lenders understand deployment challenges and will work with your designated representative.

Can my Statement of Service Letter replace my Certificate of Eligibility?

No. You need both as these separate documents have different purposes. The Statement of Service verifies your current employment. The Certificate of Eligibility confirms your VA loan entitlement based on service history.

What if the information in my letter is incorrect?

Request corrections immediately. Errors on service dates, rank, or income can delay or derail your loan approval. Never submit inaccurate documentation.

I’m in the National Guard. Are there special requirements for my letter?

Yes. Guard members’ letters should specify whether you’re on Title 10 or Title 32 status, detail your drill schedule, and indicate any upcoming activations or deployments.

Can my lender help me get this letter?

While lenders can’t obtain the letter for you, experienced military lenders like South Texas Lending can provide templates and specific guidance on what information must be included.

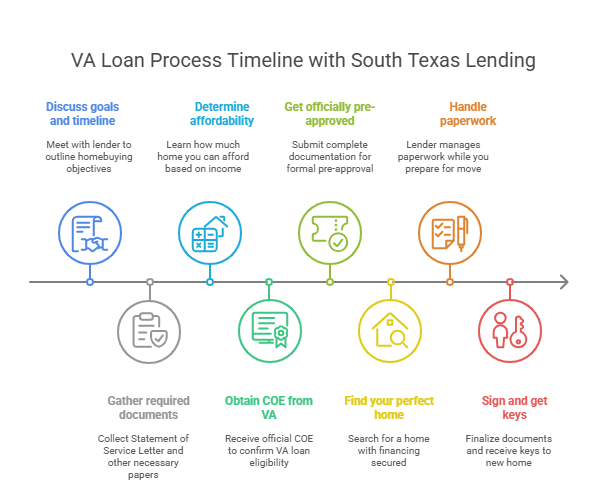

The VA Loan Process Timeline

When you work with South Texas Lending, here’s what to expect:

- Initial consultation: Discuss your homebuying goals and timeline

- Documentation preparation: Get guidance on obtaining your Statement of Service Letter and other required documents

- Pre-qualification: Learn how much home you can afford based on your military income and benefits

- Certificate of Eligibility: We’ll help you obtain your COE from the VA

- Pre-approval: Get officially pre-approved with your complete documentation package

- Home shopping: Find your perfect home with confidence in your financing

- Loan processing: We handle the paperwork while you prepare for your move

- Closing: Sign the final documents and get the keys to your new home

Active-duty service members who follow our documentation guidelines typically close 30-45 days after finding their home.

Next Steps for Your VA Loan

Ready to move forward with your VA home loan? Here’s how to get started:

- Check eligibility: Use our military loan calculator to see how much home you can afford based on your benefits

- Talk to a VA Loan Specialist: Call 210-750-6461 to discuss your options and specific situation with our military lending team.

- Get pre-qualified: Start the process online. You’ll hear back from us within 24 hours.

We know the paperwork can feel overwhelming, but you don’t have to go through it alone.

At South Texas Lending, we’ve helped thousands of active-duty service members and veterans successfully navigate the VA loan process. We’re here to help you every step of the way.